CREATE THE PLAN YOU NEED FOR THE RETIREMENT YOU WANT

Define your goal and craft a plan

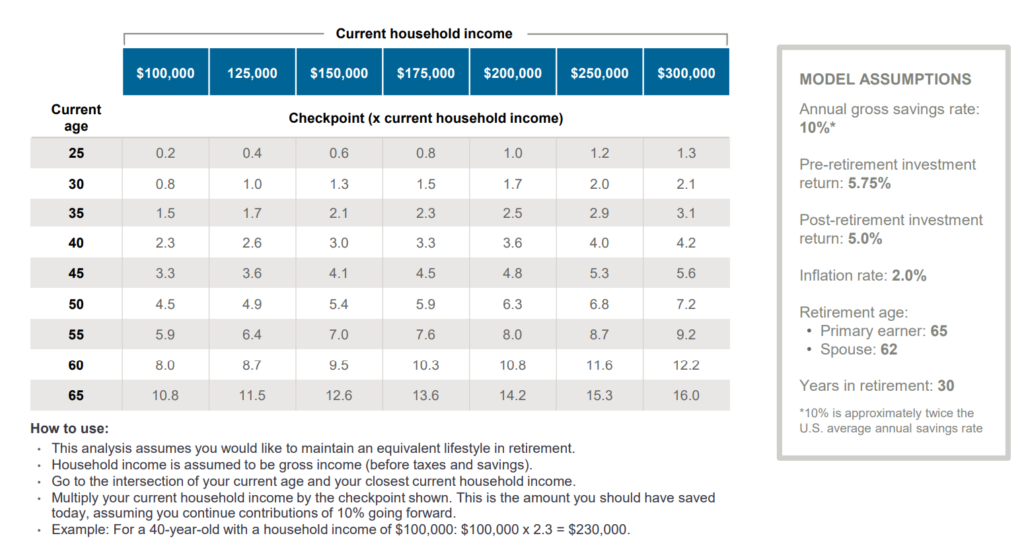

A retirement plan doesn’t have to be daunting—it’s important to just get started. This chart can help you determine if you are generally on the right path using the assumptions outlined on the right side of the page. The next step is to develop a plan that will take your own situation into account. Once you know where you’re heading, a comprehensive retirement plan is like any good GPS. It helps you get and stay on track to your destination—even as your life, the markets and the economy change.

The retirement savings checkpoint tells you how much you should have invested today to be on pace toward maintaining your current lifestyle through 30 years of retirement. If you’re below your checkpoint today or have a different vision for your retirement, you may need to work with a financial professional to adjust your plan. Be sure to review and update it regularly.

Save, save, save

A key factor in achieving a successful retirement is to save as much as possible during your working years. Your checkpoint assumes that you save 10% of your gross annual income each and every year—nearly twice the average annual savings rate in America. The good news is that you are in complete control of how much you save, and your employer may help with a company match, so make savings a priority.

PLAN FOR A LONG LIFE

The longer you live, the longer your investments must last

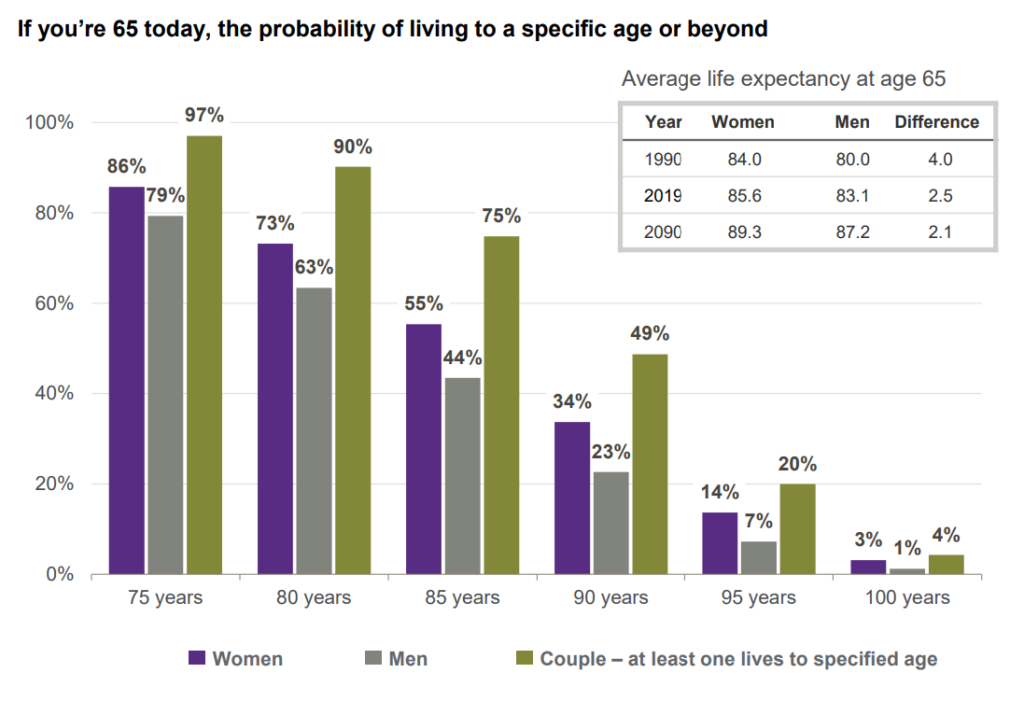

At least one member of a 65-year-old couple has a 90% chance of living to 80 or beyond, a nearly 50/50 chance of reaching 90 and a one-in-five chance of turning 95 or older. Living longer affects key retirement decisions such as how to make the most of your time, how to invest, when to claim Social Security and whether you might need long-term care.

If you’re in good health at 65 and have a family history of longevity, your retirement plan should account for 30 or more years of living expenses. And keep in mind that with new medical advances, family history is not destiny, so you may live longer than you think. That means your investments need to continue growing long after you stop working to keep pace with inflation and reduce the risk of outliving your money.

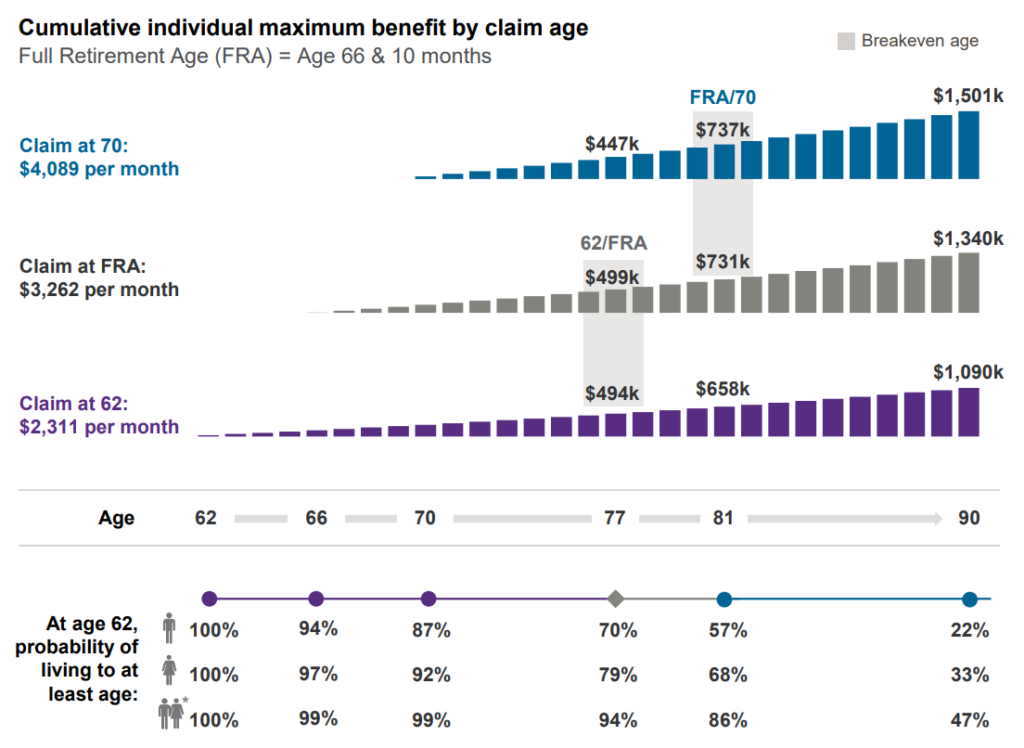

MAKE AN INFORMED DECISION ABOUT SOCIAL SECURITY (PART 1)

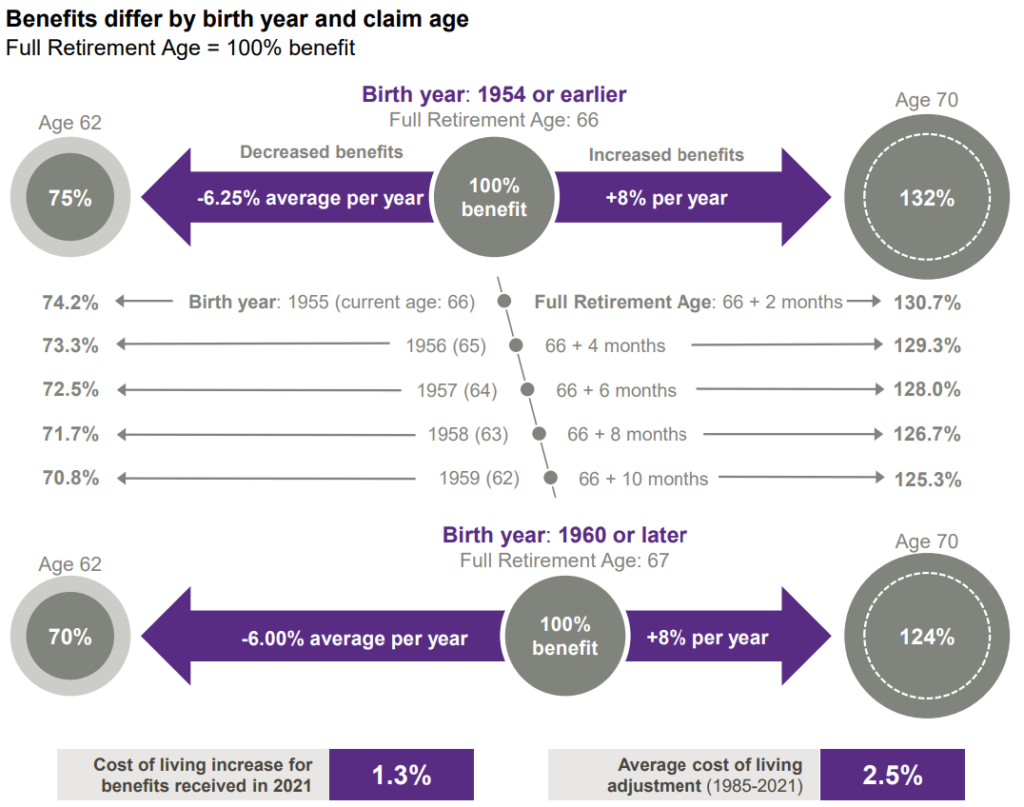

Social Security pays you more for waiting

Social Security benefits are calculated based on your 35 best earning years. You are eligible for 100% of your benefit at your Full Retirement Age (FRA). Individuals born in 1960 and later have an FRA of 67. Claiming at 62 will permanently reduce your benefit by as much as 30%. Waiting to claim after FRA gives you an 8% increase each year in your benefit amount for a maximum of 124% or more.

Times they are a-changing

Individuals turning 62 in 2021 will have an FRA of 66 and 10 months as a result of the Social Security Amendments Act of 1983. This Act moves FRA 2 months each year for 6 years until it reaches and stays at age 67 in 2022. An FRA of 67 results in even less if you claim early and not quite as much at age 70.

MAKE AN INFORMED DECISION ABOUT SOCIAL SECURITY (PART 2)

How long until waiting pays off?

Should you take smaller amounts sooner? Or wait for larger amounts later and rely on your portfolio in the meantime? If your goal is to maximize your cumulative benefit, the answer depends on how long you live. You would receive more in total at age 77 by claiming at FRA (66 and 10 months) rather than 62, and at age 81 when choosing between FRA and 70.

The odds of receiving more by waiting are in your favor

Because of the relatively high probability of living to 77 and 81, delaying Social Security often pays off in the long run—especially if you are the primary wage earner of a couple and your portfolio gives you that flexibility.

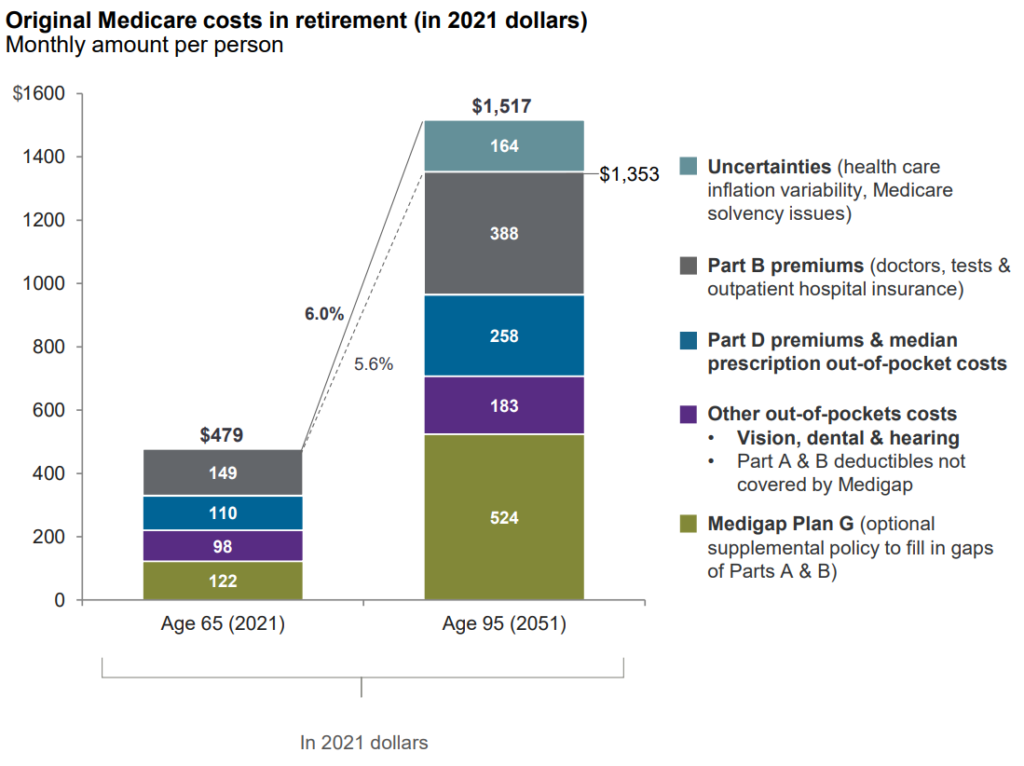

KNOW WHAT TO EXPECT WITH HEALTH CARE COSTS

Plan on rapidly rising expenses

Medical expenses tend to rise sharply throughout retirement as we grow older and require more care at higher prices. Out-of-pocket costs for an average 65-year-old retiree on traditional Medicare are projected to almost triple from around $480 per month this year to over $1,500 in today’s dollars by age 95.

These costs are averages per person and do not include most long-term care. Costs may be much higher if you have expensive prescriptions. And you’ll pay more in Medicare premiums if your income is higher.

Include health care costs as a separate expense in your retirement plan and assume a 6.0% annual growth rate to be conservative. You may want to assess your long-term care alternatives when you are healthy, or as early as age 50, when the most options are available to you.

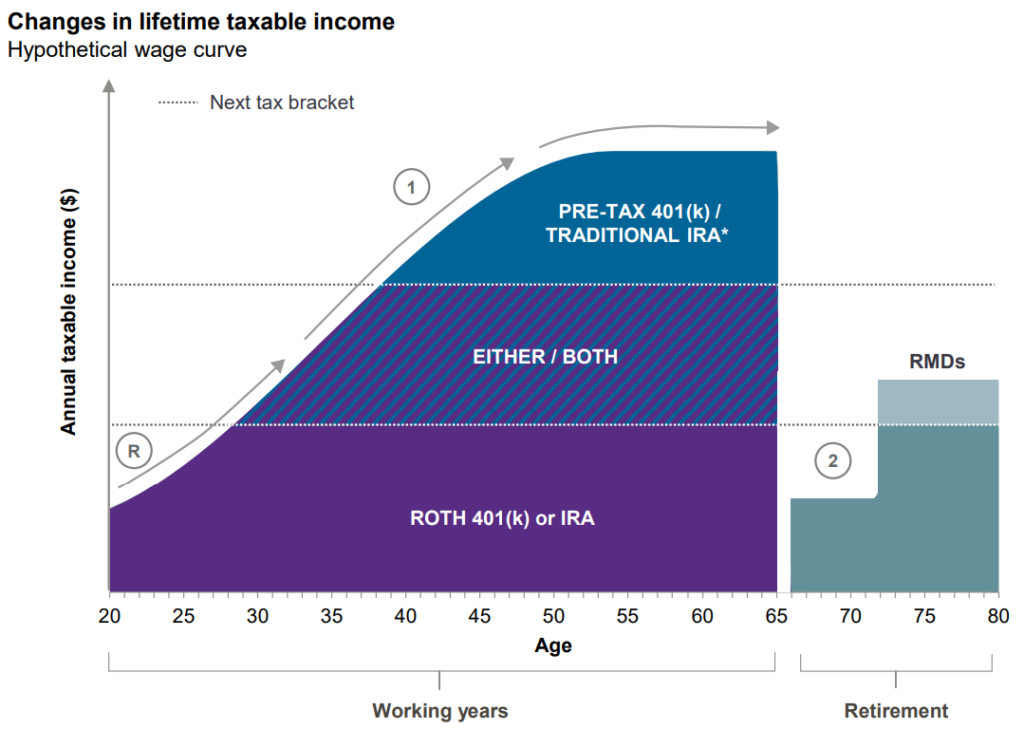

MINIMIZE TAXES TO MAXIMIZE YOUR RETIREMENT

4 Ways to pay less in taxes and keep more for retirement

- Optimize savings vehicles by opening tax-advantaged accounts (401(k)s, IRAs, HSAs) and consider diversifying across pre-tax/deductible and Roth options if available to you. As a general rule, saving into a Roth when income is relatively low and shifting as your income rises may result in lower taxes overall.

- Consider deferring income when you are in your peak earnings years until you are in a lower tax bracket in retirement. However, if you are already concentrated in tax-deferred accounts, contributing to a Roth may help you diversify your retirement tax picture.

- Work with your accountant and financial professional to actively manage your tax picture throughout retirement. Higher incomes can also affect your Medicare premiums and taxability of Social Security benefits. Consider proactive Roth conversions in years when your tax rate is low.

- Maximize your after-tax return by holding your highest-taxed investments (those generating ordinary income or short-term gains) in tax-advantaged accounts, after funding your emergency reserves. Look to offset gains with losses when rebalancing your portfolio or take withdrawals from taxable accounts.

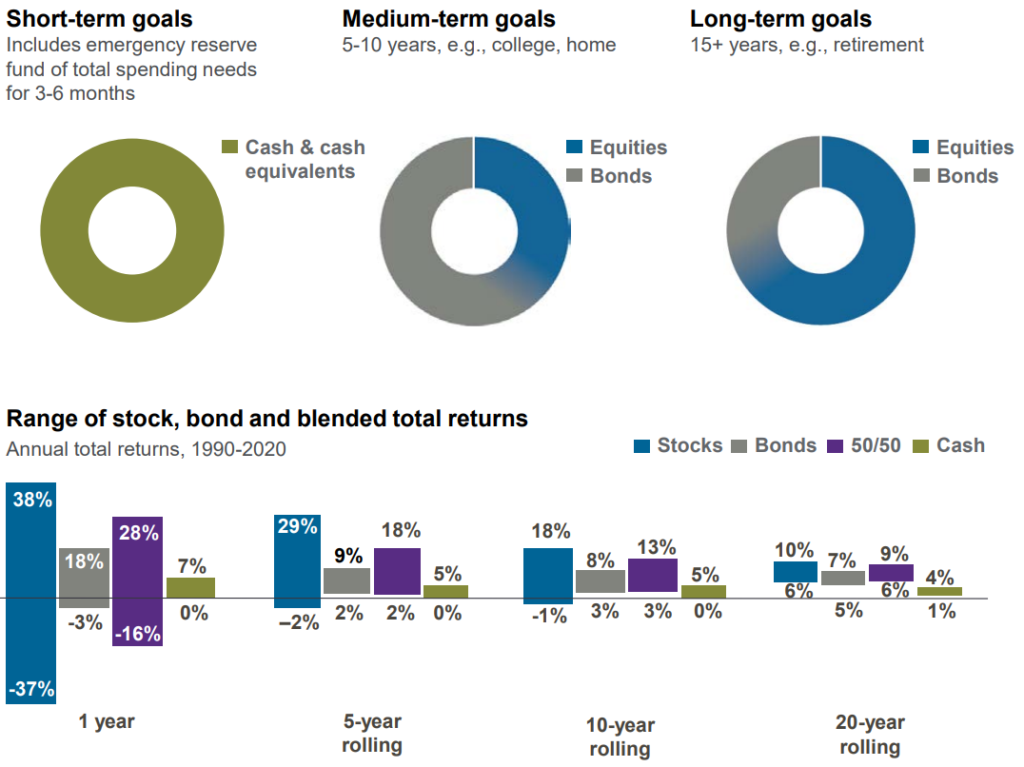

USE TIME TO YOUR ADVANTAGE WHILE PROTECTING FOR THE SHORT-TERM

Save and invest based on your time horizon

All goals are not created equal, so investing for them as one may not be the best plan. Instead, decide how much of your savings to put toward college, retirement and other goals based on your priorities. Next, create an investment strategy that allows you to take advantage of the longer investment horizon for goals with longer time frames. To keep your strategy on track, be sure to have a short-term fund that can cover emergencies without having to sell your investments during down markets.

Good things come to those who wait

While markets can always have a bad day, week, month or even year, history suggests investors are less likely to suffer losses over longer periods.

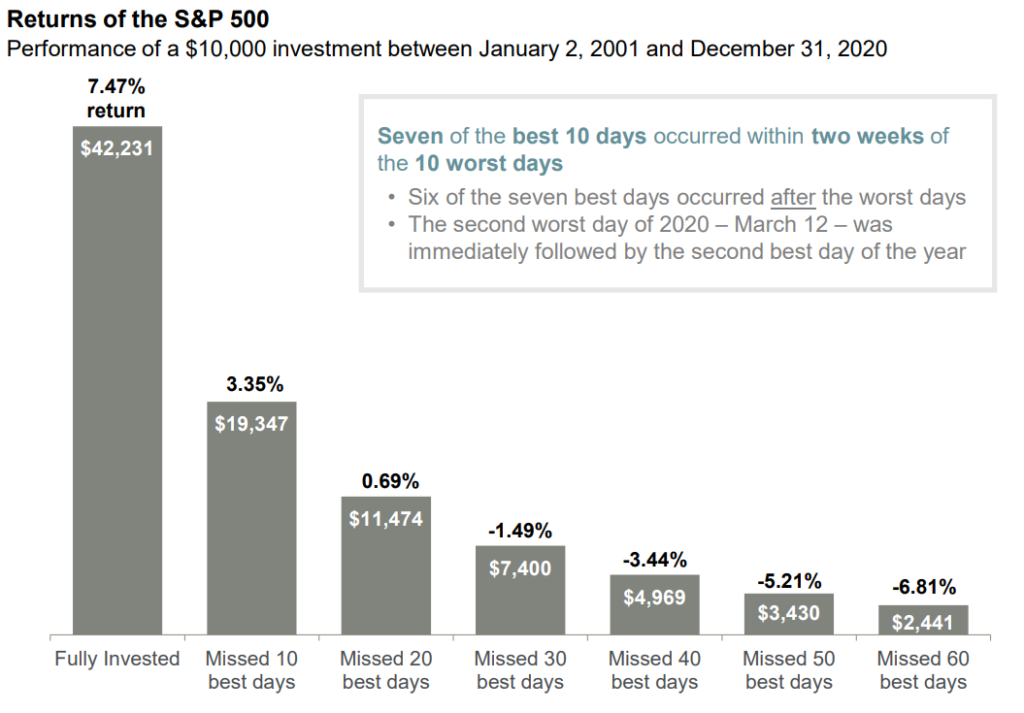

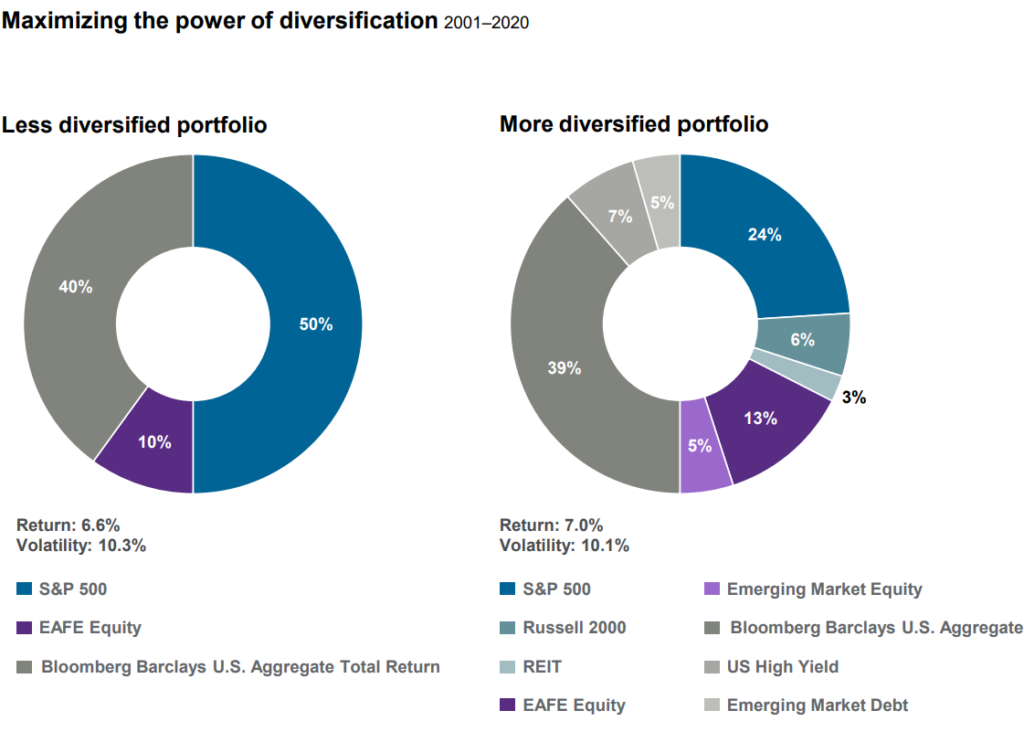

BE WELL DIVERSIFIED AND STAY INVESTED (PART 1)

Get help from a financial professional to create a diversified strategy

With the help of a financial professional, create an investment strategy that will help you maximize return while also taking a certain level of risk into account. The strategy on the right is more diversified – meaning it uses a wider range of asset classes than the portfolio on the left. From 2001-2020 each strategy has experienced the same level of risk (as measured by standard deviation or “volatility,”) but the more diversified strategy experienced a higher return.

BE WELL DIVERSIFIED AND STAY INVESTED (PART 2)

Plan to stay invested

During periods of extreme market declines, a natural emotional reaction can be to “take control” by selling out of the market and seeking safety in cash. This is due to “loss aversion” – or the fact that losses hurt more than gains feel good. The action not only locks in losses but often results in missing some of the best days that closely follow that are key to a portfolio’s recovery.

Staying the course with a diversified long-term investment strategy is likely to produce a better retirement outcome.