Plan sponsor pain points often revolve around three things: taxes, liability and costs. Sponsors that pay their 401(k) expenses out of company assets rather than plan assets can potentially get help with all three:

1. Bigger tax deduction

2. Reduced fiduciary liability

3. Lower participant fees

One way to tell if a 401(k) plan is successful is to set measurable objectives for participant outcomes. The following hypothetical example shows how plan expenses can be part of that mix.

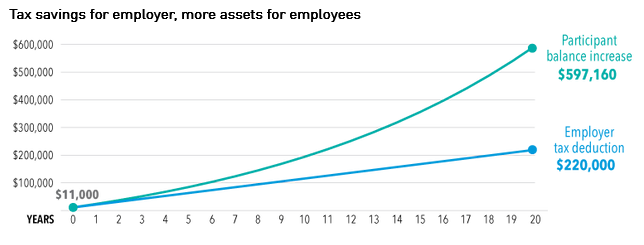

Tax savings for employer, more assets for employees

Example assumes annual recordkeeper costs of $4,000, advisor costs of $5,000 and TPA costs of $2,000, totaling $11,000, that are added to principal at an interest rate of 8% over 20 years, with compounding done four times annually. This example was developed by third-party retirement plan consultant Pat Shelton, GBA and managing member of Benefit Plans Plus, LLC. For illustrative purposes only and not intended to portray actual investment results.

In this example of a relatively small 401(k) plan, the employer receives an $11,000 annual tax deduction and participants receive a cumulative addition of more than $597,000 to their account balances over 20 years. This additional accumulation may really make a difference in the quality of retirement for participants. Sponsors, of course, can elect to pay or not pay plan expenses each year, depending on business conditions.

The benefits for employees is obvious, less fees equals higher account balances over time. Many plan sponsors have not reviewed fee models that allow them to pay for all or some of the expenses of their employer retirement plan. Some of the potential benefits include:

Plan fees are a tax-deductible expense. In many cases, the largest account balances pay the most fees. Typically who are these people? Usually they are the owners, executives, top sales people, etc. This is a benefit to all employees but also a huge benefit for key employees.

Reduces the risk of excessive fees. When a company decides to pay some or all of the plan cost, a smart 401(k) plan will run with zero revenue sharing funds and will find the expense ratios dramatically reduced for plan participants. This is a subtle benefit that most employees probably won’t notice, but also reduces the chances of getting tangled up in a legal battle over plan fees.

Transparency typically offers better pricing. When a company negotiates cost on behalf of the retirement plan and wants to use funds that do not pay any of the providers involved to run the plan, it usually leads to lower pricing. It forces the plan providers to fully disclose their cost and how they calculate the cost. This allows plan sponsors to accurately compare providers and negotiate pricing. In my opinion, this is the future of retirement plan pricing and can be done no matter who pays the plan cost, employer or plan participant.