According to the Bureau of Labor Statistics, today’s median bachelor’s degree recipient receives $1,281 in weekly earnings compared to the $749 made by a typical high school graduate.1 Clearly, one of the best investments you can make for your children is an investment in their educational future.

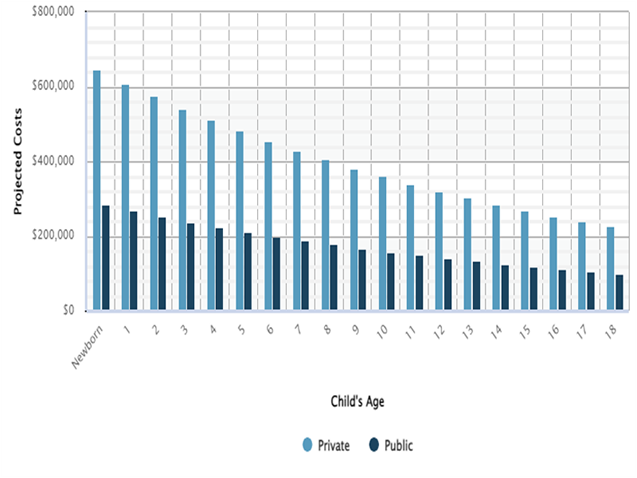

You may think that setting up a bank savings account for your newborn’s education will get him or her off to a great start. You might, however, want to think again. According to 2021 data from the College Board, the projected average cost for your newborn’s four-year degree at a public college could total over $283,000. And should your child decide to attend a private college, the total could be over $645,000.2

But don’t despair yet. Even without time on your side — if your children are teenagers, for example — a sound investment strategy, coupled with knowledge of other college financing options, may put your children on the road to a valuable four-year college degree.

Assumes a 6% annual increase and current one-year cost of a four-year public ($22,690) and four-year private ($51,690) college. Source: ChartSource®, DST Retirement Solutions, LLC, an SS&C company. Based on data published by the College Board for the 2021-2022 academic year. Chart is based on hypothetical growth rates. Your results will vary. © 2022 SS&C. Reproduction in whole or in part prohibited, except by permission. All rights reserved. Not responsible for any errors or omissions. (T11A)

A Sound Strategy

As with any large financial goal, it’s good to start investing early and often for college. First, set your goal: figure out how much you will need to save for each child based on his or her age (see accompanying chart). Then, develop an investment plan and stick with it. Consider discussing the following guidelines with your financial professional when developing your plan.

Goal: Final Tuition Bill Due in 12 to 22 years

With time on your side, your portfolio can potentially withstand a bit of volatility in your quest for higher returns. Stocks have historically provided the greatest long-term growth potential. Of course, past performance can’t guarantee future results. You must remember the volatility involved in stock investing and consider your ability to wait out potential fluctuations in the value of your child’s college investments.

Goal: Final Tuition Bill Due in 8 to 11 Years

In addition to keeping your portfolio aimed toward growth with stocks and stock mutual funds, you might want to add or increase a fixed-income element to balance risk. Also, now is probably a good time to teach your child about investing — by encouraging that a portion of the dollars earned through paper routes and babysitting be contributed to the college investment plan.

Goal: Final Tuition Bill Due in Less Than 8 Years

You may start allocating more of your portfolio to fixed-income and money market investments. If you have virtually nothing saved, you have a challenge ahead of you, but some cost-cutting in other areas of your life might allow you to make substantial monthly investments. The less you have saved, the more you may need to be aggressive in your investments in seeking higher returns, as long as you have the appropriate risk tolerance.

Considerations

Although many investments, including stocks and bonds, have traditionally outpaced savings accounts in terms of performance, past performance cannot guarantee future results. Bear in mind that unlike savings accounts, investments are not insured by the Federal Deposit Insurance Corporation (FDIC); therefore, your investments’ value may fluctuate a great deal over time and could even result in a loss. Also remember that any investment plan needs a fresh look every year or so to determine if adjustments need to be made. Generally, changes should be made as your time horizon narrows, the day nears when you will send your child off to college, and preservation of principal becomes a primary concern.

Other Financing Options

Beginning your investment plan by considering the time frame available to you is probably your best bet in seeking to meet college costs. In addition, consider these options:

- Encourage savings gifts: When relatives ask what your children want for birthdays or holidays, encourage gifts that will help finance their education. Though it may not be a child’s first choice now, they’ll thank you later. Such gifts include Series EE Savings Bonds; shares of a mutual fund given through the Uniform Gifts/Transfers to Minors Acts (UGMA/UTMA); and zero-coupon bonds that mature in a given year around college enrollment. Parents or others can contribute up to $2,000 annually (per child, and if certain income restrictions are met) to a Coverdell Education Savings Account (formerly called an Education IRA) where any earnings can accumulate tax free and withdrawals can be made federal (and possibly state) income tax free for qualified education expenses. An individual can make annual gifts of up to $16,000, gift tax free, to a minor under UGMA/UTMA. And friends and family can pay any amount directly to a youngster’s college for tuition and fees, with no gift tax consequences. Remember to brief yourself on the tax considerations of each of these gifts (and speak with your tax professional) so you’re not caught off guard by Uncle Sam.

- Section 529 plans: These state-sponsored plans allow individuals to invest in a predetermined investment pool and offer some flexibility on when you can contribute. Withdrawals for qualified higher education expenses and tuition at an elementary or secondary public, private, or religious school, are federal income tax free. Withdrawals may also be free of state income taxes for residents of states that allow this benefit.

- Apply for financial aid: Each year, there are millions available in financial aid from a variety of organizations and scholarship funds. Even if you think you’re ineligible for financial aid, complete the applications and mail them in on time.

- Don’t rule out less expensive schools: Public universities and community colleges can be among the best options. Higher education is certainly one area where most expensive does not necessarily mean best.

- Develop networks and ask questions: High school guidance counselors, religious and civic organizations, and the colleges your child applies to can all provide good leads for additional sources of scholarships, grants, and loans.

Together, time and a smart investing strategy can help you meet the rising costs of higher education. Combine that bet with a little creativity and a lot of information, and you can help provide your children with an investment that no one can take away: a college education.

1Source: Bureau of Labor Statistics (BLS), TED: The Economics Daily, October 21, 2019. Data from BLS Population Survey.

2Sources: SS&C Technologies, Inc.; the College Board, 2021. Cost estimates are based on the 2021-2022 academic year and assume that costs increase by 6% annually. Figures include tuition, fees, and room and board. Keep in mind that unlike money market investments, which involve risk and possible loss of principal, bank savings accounts are FDIC-insured.