With an unpredictable future, infinite information, and intense competition, success in the markets has never been more difficult. The hurdle for good decision making is high. Three fundamental principles reinforce a wise approach to smarter decisions and better outcomes: risk management, diversification, and behavior. An appreciation of each increases our chance of financial success.

1. Prioritize Risk Management

Our money lives are typically framed in terms of achieving more. It’s a legitimate quest, we must compound our savings at a rate in excess of inflation in order to maintain or improve our living standards, but a truly successful financial plan prioritizes risk management over return enhancement.

-

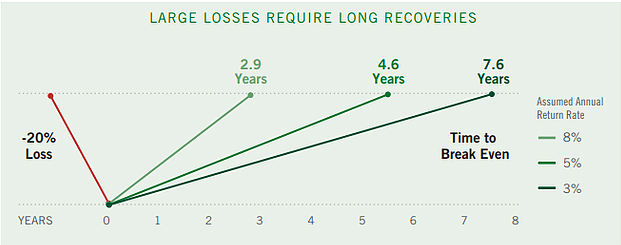

The first reason for this is mathematical. As the graphic illustrates, negative compounding is a nasty affair: Losses can require an exceptionally long recovery time just to get back to scratch.

-

The second reason is emotional. According to the psychological principle of “loss aversion,” losses loom much larger in our psyches than gains. Researchers suggest a 2:1 ratio: A $100 loss is twice as painful as a $100 gain is pleasurable. Because investing is a decades-long process and not just a final outcome at, say, the age of retirement, it ends up that much of what we want to do along the way is minimize regret, not maximize returns.

Taking risk is a balancing act. We must risk our capital to achieve growth, but not so much as to invite paralyzing losses. And, as precise and technical as “risk management” sounds, it’s actually more mindset than algorithm. Money mistakes, will happen, but we can try to set ourselves up to recover and thrive after the dust has settled.

2. Embrace Diversification

The future is unpredictable. Though not a controversial idea, it doesn’t jibe well with the human need for certainty. Part of our deeply ingrained survival instinct is that the world around us needs to make sense, and part of that engagement involves anticipating a variety of future events. We don’t deal well with nuanced probabilities, and instead tend see the future in an either/or frame, up or down, will or won’t, heads or tails.

Investing is a bet on an unknowable future. Sure things and short cuts don’t exist when it comes to healthy long term finances. So we diversify. We spread our bets. We build a portfolio with exposures to different sources of risk on the theory that such a portfolio will not produce maximum possible returns but instead those that are optimal, gains that fulfill our goals without overextending on risk to get there. The quest for maximum returns violates our first principle of risk management.

Diversification is the green vegetable of money life. Just because it’s healthy doesn’t mean we like it. By definition, diversification means that there will always be something in our portfolios that is losing or lagging. We will have an urge to move our capital to what’s “working”—the exact opposite of what we should do according the basic principle of buy low and sell high. Diversification isn’t always comfortable, but it remains the soundest approach to building our portfolios.

3. Control Behavior

Ultimately, our long-term investment results are driven by our behavior, including how we respond to life’s inevitable ups and downs. As the legendary investor Benjamin Graham wrote, “The investor’s chief problem and, even his worst enemy, is likely to be himself.”

Humans are hardwired with a litany of emotional and cognitive biases:

-

We are overconfident in our skills and opinions.

-

We fail to challenge our own beliefs, even when in error.

-

We overweight the relevance of information most recently seen.

-

We uncritically mimic the decisions of others.

Thus, we sometimes make regrettable choices. Abundant data prove that we tend to underperform our own investments because we buy and sell at the wrong times. This “behavior gap” can and does hurt long-term goal fulfillment.

It’s a focus on calm, patient decision making in the context of a well-defined financial plan that will keep investors in relatively good stead. That might be found in better individual discipline. Systematizing sound decisions (such as through an automatic savings plan) and/or relying on a coach are also valuable wellsprings of long-term success.

In modern markets, we are drowning in information, but thirsty for wisdom. The three pillars discussed here, risk management, diversification, and behavior, are hardly an exhaustive list of everything we need to know. But together, they form the core of a sound investment philosophy which should help us find clarity and balance.