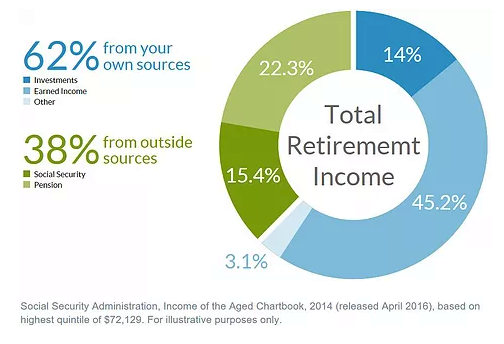

Before anyone can embark on building a practical road map to financial security, everyone needs to understand five key risks that can potentially derail a lifetime income plan. Many people counted on Social Security and pension benefits to cover their retirement income needs. But today, retirees will be more personally responsible for funding their own retirements.

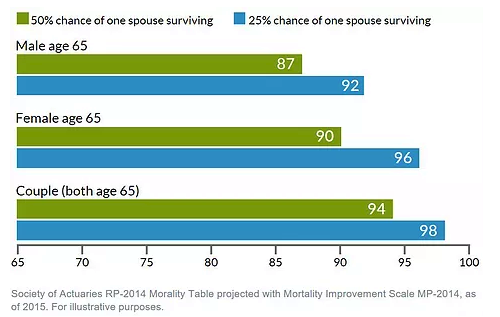

1. Plan for living longer than you think

A retirement income plan may help to ensure that your assets last as long as your retirement. When thinking about how long you might need income, many people tend to think in terms of life expectancy. But statistically, half of the population will live longer than their expectancy, which means that they will underestimate how long they will need their savings to last.

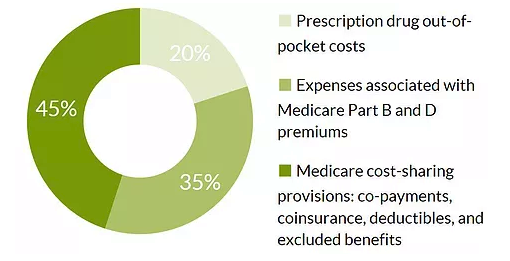

2. Saving for rising health care costs

Longer life spans, rising medical costs, declining employer-sponsored medical coverage, and possible shortfalls ahead for Medicare all add up to make health care expenses a critical challenge for retirees and pre-retirees alike. In fact, a 2017 Fidelity study estimates that a couple retiring today at age 65 may need current savings of approximately $280,000 to supplement Medicare and cover their out-of-pocket health care costs in retirement.

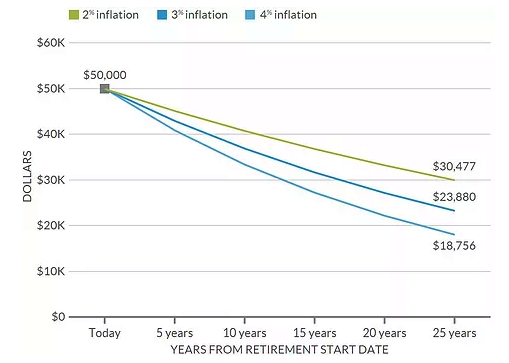

3. Even low inflation could damage purchasing power</div><div>Inflation is the long-term tendency of money to lose purchasing power. And it can have a particularly negative effect on retirees because it chips away at retirement income in two ways:

- Increases the future cost of goods and services

- Potentially erodes the value of assets set aside to meet those costs

4. Retirees need stocks for the long haul

Some people fear losing their nest egg, so they avoid stocks and stick with fixed-income investments. But by doing this they give up long-term growth potential and risk outliving their money.

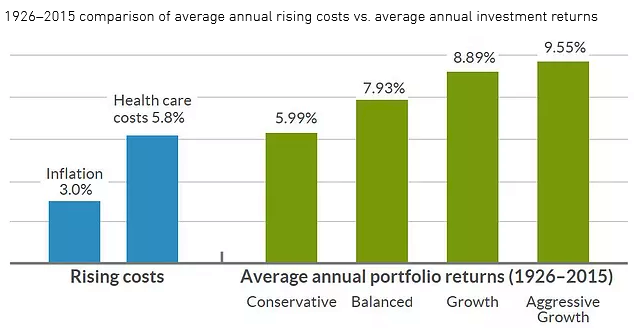

1926–2015 comparison of average annual rising costs vs. average annual investment returns

- Data for health care costs is from the Centers for Medicare and Medicaid Services, National Health Expenditures Estimates 2018–2025.

- Examples of target asset mixes designed to meet various goals–Conservative: 20% stocks,† 50% bonds, 30% short-term; Balanced: 50% stocks,† 40% bonds, 10% short-term; Growth: 70% stocks,† 25% bonds, 5% short-term; Aggressive Growth: 85% stocks,† 15% bonds.

- Stocks are composed of domestic and foreign stocks.

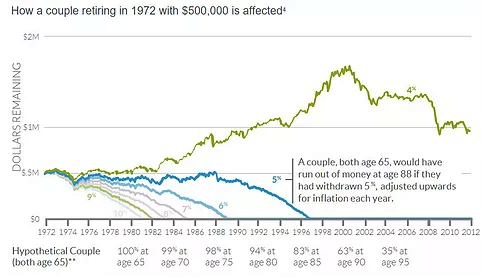

5. Sustainable withdrawal rates can extend the life of a portfolio

Even the savviest asset allocation strategy can misfire without an equally wise strategy for withdrawing assets. The withdrawal rate can dramatically affect how long the money will last.

- For charts which highlight varying levels of stocks, bonds, and short-term investments, the purpose of these hypothetical illustrations is to show how portfolios may be created with different risk and return characteristics to help meet a participant‘s goals. You should choose your own investments based on your particular objectives and situation. Remember, you may change how your account is invested. Be sure to review your decisions periodically to make sure they are still consistent with your goals. You should also consider all of your investments when making your investment choices. All index returns include reinvestment of dividends and interest income. It is not possible to invest directly in any of the indices described above. Investors may be charged fees when investing in an actual portfolio of securities, which are not reflected in illustrations utilizing returns of market indices.

- Probability of a couple surviving to various ages is based on Annuity 2000 Mortality Table, Society of Actuaries. Figures assume a person is in good health.